Residential landlords may well have felt an obligation or need to afford their tenants leniency as regards paying rent to help support them through the current pandemic, and they may well expect to see this year’s tax liabilities reduce as a consequence. However, measures announced in the Summer Budget 2015 regarding tax relief for finance costs take full effect this year, potentially leaving landlords with reduced income and, dare I say it, increased tax liabilities.

Generally, calculating the profits of a letting business follows the same rules as any other trading business, but with effect from 6 April 2017, it has been necessary to make a distinction between individuals letting residential property and those letting commercial property.

For those letting residential property, tax relief for finance costs has been restricted, albeit with the restriction phasing in gradually year-on-year whereby the costs allowed as a letting expense have decreased in favour of a basic rate tax credit on the balance:

- in 2017/18 the letting expense was restricted to 75% of finance costs with a basic rate tax credit being given on the remaining 25%

- in 2018/19 only 50% of finance costs were given as a letting expense and 50% attracted a basic rate tax credit

- in 2019/20 only 25% of finance costs were given as a letting expense and 75% attracted a basic rate tax credit

- from 6 April 2020 all finance costs incurred by a residential landlord will generate tax relief only by way of a basic rate tax credit

To illustrate the effect of the above, let’s consider an individual with a job earning a salary of £70,000 and in addition:

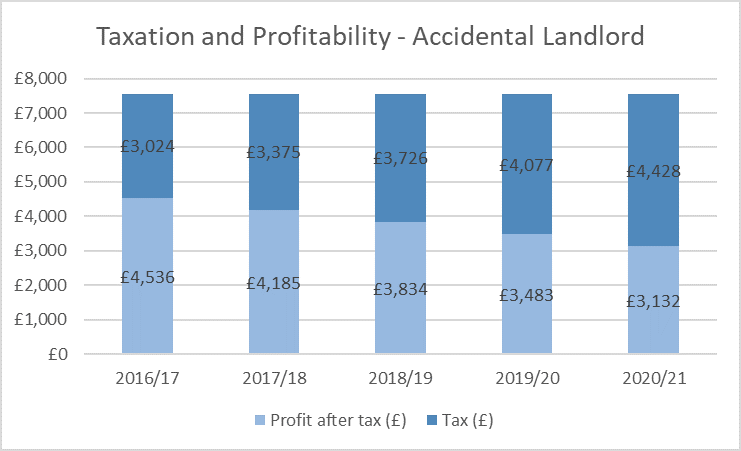

- As an unintentional landlord, perhaps letting out their former home after moving in with a partner, earning a monthly rent of £1,300 with mortgage interest of £585 and other monthly running costs of £85, they will see their tax liability increase by about £1,400 as a result of the 2015 measures.

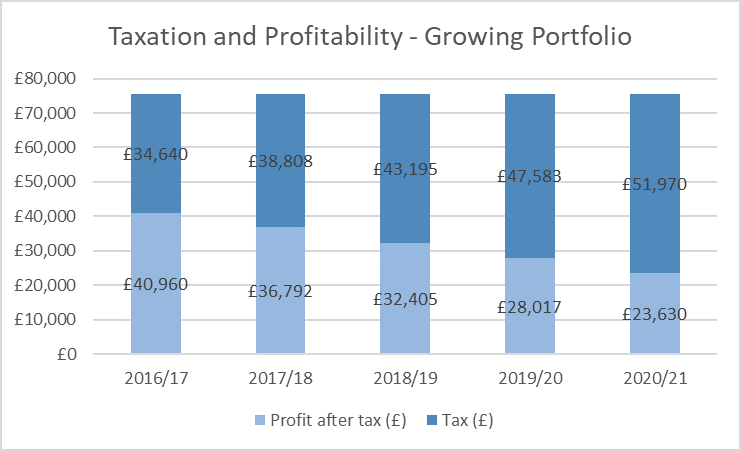

- With a growing portfolio of, say, ten properties let on the same basis as above, the individual is likely to see their tax liability increase by about £17,500.

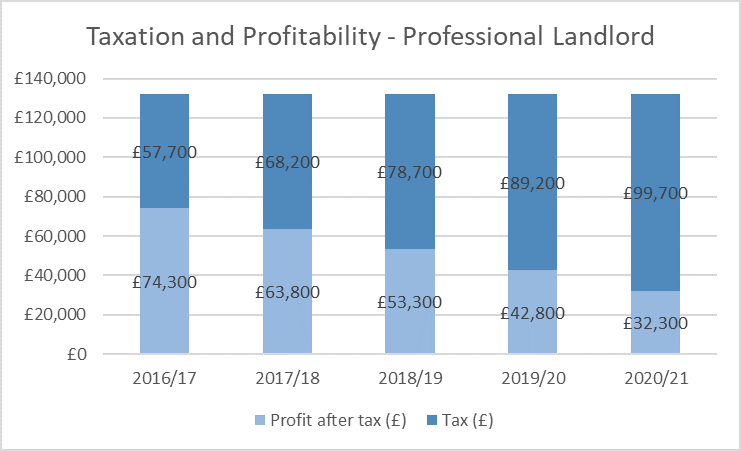

- As a professional landlord, having reduced their salary to £40,000 in favour of growing a property portfolio generating monthly rents of £30,000 with associated finance costs and running costs of £14,000 and £5,000 per month respectively, they are likely to see an increase in their tax liability of about £42,000 comparing the 2016/17 ‘as-was’ position and the current position.

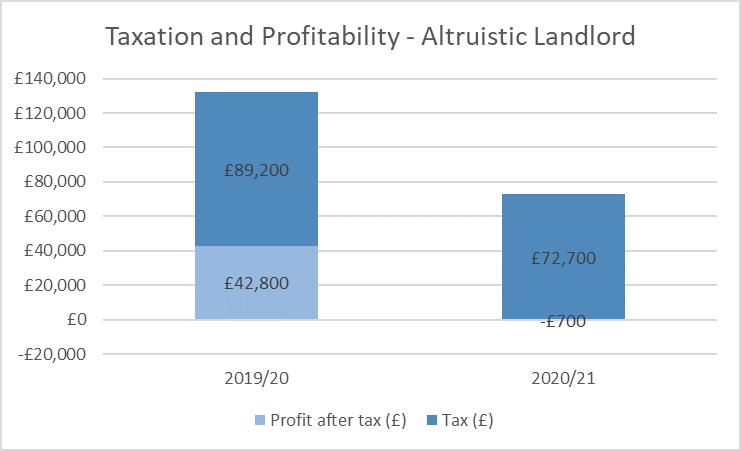

- And let us assume the professional landlord is an altruistic individual granting tenants a two-month rent holiday, which doesn’t increase their tax liability as such, but it does mean all profits earned this year – together with about £1,000 of their net salary – will go towards paying tax on rental profits that, in the real, world don’t exist!

The illustrations above consider only the direct income tax cost of the 2015 measures on rental profits, but there is a raft of knock-on implications that can make an individual’s position much worse, for example:

- Reduced child benefit entitlement

- Increased student loan repayments

- Investment income and capital gains being pushed into the higher tax brackets

- Further abatement of the personal tax-free allowance

- Increased tapering of the pension savings annual allowance

Now that the 2015 provisions are in full effect, if you’re a residential landlord, or if you advise residential landlords, its crucial that you understand how measures introduced five years ago will impact upon tax liabilities in the current year and going forward.

Understanding tax exposure in the current year and advising on steps that can be taken to lessen the impact of the 2015 measures is something we can help you with; tax leakage is just another expense of your rental business and one that should be understood, managed and reduced where at all possible.